A prominent short seller who is suing Tesla and Elon Musk for manipulating its stock price says the company would be better off without Musk as the CEO.

Andrew Left, the founder of Citron Research, told CNN’s Julia Chatterley on “First Move” Tuesday morning that it might make sense for Musk to have a more strategic or visionary role at Tesla(TSLA). He said the company could bring in someone else to run the day to day operations.

Left said it would have seemed like “death to the company” a few months ago to think Tesla might need someone else to run it. But Musk has courted controversy as of late. Recently Musk has smoked marijuana during a video interview and accused a caver in the Thai rescue of a stranded soccer team of being a pedophile.

Last week, Left filed a class action lawsuit that accuses Musk of securities fraud after he tweeted in August that he had “funding secured” for a plan to take Tesla private at $420 a share. Musk has since abandoned the plan.

Left argued that the tweet was an attempt to “burn” short sellers who are betting against the company.

“Musk has a long-standing public feud with short-sellers and often uses his personal Twitter account to taunt and confront skeptics of his company,” Left noted in the lawsuit.

On Tuesday, Left conceded that his short position on Tesla has been wrong so far. The stock, despite recent volatility, has soared over the past few years.

“Rumors of their death have been greatly exaggerated and talked about many times,” Left said,

But Left told Chatterley he thinks that at the end of the day, Tesla is going to need more cash and it will probably have to sell more stock to raise funding.

That would be bad news for existing shareholders. Shares fell 2% Tuesday and are now down more than 20% in the past month.

CNNMoney (New York) First published September 11, 2018: 11:54 AM ET

If you’re nearing retirement age and your savings are looking a little sparse, you’re not alone. Forty-six percent of baby boomers don’t have anything stashed away for retirement, according to a study from the Insured Retirement Institute, which means nearly half of soon-to-be retirees need to supercharge their savings if they don’t want to work the rest of their lives.

The bad news is that if you’re in your 50s and are just now starting to save, it’s going to be a tough road ahead to save enough to enjoy a comfortable retirement. The good news is that it can be done, and even if you can’t save half a million dollars by the time you turn 65, you can put away a decent chunk of change — which is far better than nothing.

Picking up steam after a late start

One advantage workers in their 50s have over younger employees is the benefit of catch-up 401(k) and IRA contributions. If you’re under age 50, the 2018 annual contribution limit for 401(k)s and IRAs is $18,500 and $5,500, respectively. But for those age 50 and over, the annual limits are $24,500 and $6,500.

While that’s a fantastic benefit to take advantage of if you can, chances are if you’re struggling to save for retirement, it’s not going to be feasible to suddenly start saving nearly $25,000 per year. In that case, the best thing to do is determine what you can save, set a goal for yourself, and stick with it.

The first step is to create a thorough budget of all your monthly expenses to see where your cash is going and how much you have left to save at the end of the month. This is also a good time to see where you can make cuts. Be honest with yourself here to decide how important these expenses are compared to retirement. Ask yourself if you absolutely have to be eating out every week or whether you really need to take the family on a fancy vacation each summer. If you’re especially serious about saving, you may even choose to downsize to a smaller home to potentially save hundreds of dollars per month on your mortgage.

Once you know roughly how much you’ll have to contribute to your retirement fund each month, start crunching some numbers. Retirement calculators are helpful in giving you an estimate of how much your savings will amount to by the time you retire as well as how much you’ll likely need to have saved by retirement. Keep in mind that these numbers are just estimates, but they can give you a rough idea of where you stand and how long your savings will last.

If your numbers aren’t where you want them to be, don’t get discouraged. Saving is hard work, and beating yourself up over the fact that you didn’t start saving earlier won’t make it any easier. If you’ve trimmed your monthly expenses as much as you can and are still struggling to save, you have a couple other options.

Making the most of Social Security

One option to consider is to delay claiming Social Security benefits, which will result in fatter checks each month. You’re able to start claiming benefits as early as age 62, but for every year you delay past your full retirement age (FRA), or the age at which you receive 100% of the benefit amount you’re entitled to, you’ll receive a boost in benefits. For example, if your FRA is 67 and you wait to claim until age 70, you’ll receive an additional 24% on top of the full 100% you’re entitled to.

If you’re already going to be strapped for cash during retirement, this extra money can make a major difference. For example, say your FRA is 67 and the full amount you’re entitled to (or the amount you’ll receive if you wait until age 67 to claim) is $1,200. If you instead delay claiming until you reach age 70, you’ll be receiving $1,488 per month. An extra $288 per month may not seem like a significant difference, but it adds up to nearly $3,500 over a year — which is a lot of money when you’re trying to make each dollar count.

In addition to waiting to claim Social Security, you can also put off retirement by a few years and continue working as long as you can. This isn’t the most exciting option, but it can help you save a lot of money in a relatively short period of time. Because not only are you continuing to contribute to your retirement fund as you work, you’re also not draining your savings just yet.

For example, say you’re 50 years old with zero savings and you want to retire at 65. If you’re contributing $300 per month and earning a 7% annual rate of return on your investments, you’ll have a total of $93,859 saved after 15 years. While that’s a good amount of money (and far better than nothing), it will likely only last you a few years during retirement. If, however, you delay retirement by 10 years and work until 75, continuing to contribute $300 per month earning a 7% return, you’ll end up with $236,241. And if you also wait until age 70 to claim Social Security, you’ll receive a boost in benefits there as well.

If your employer offers matching 401(k) contributions, you stand to earn even more by working a few more years. In this situation, if your employer matches your $300 monthly contribution, bringing your total contributions to $600 per month, you’ll end up with $472,482 by age 75, compared to just $187,718 had you retired at 65.

Related links:

• Motley Fool Issues Rare Triple-Buy Alert

• This Stock Could Be Like Buying Amazon in 1997

• 7 of 8 People Are Clueless About This Trillion-Dollar Market

When you’re behind on your savings and can see retirement looming on the horizon, it’s easy to want to give up on your financial goals. But it is possible to enjoy a comfortable retirement even if you got a late start on saving, because a little planning and a lot of determination can go a long way.

CNNMoney (New York) First published September 28, 2018: 10:47 AM ET

Dreaming of handing in your notice at work and joining the ranks of the retired?

Retirement can be wonderful — if you’re prepared for it. So before you put an end to your career, it’s essential to make sure you’re 100% ready.

Not sure how to do that? Taking these five steps can put you on the path to a happy and secure retirement.

1. Coordinate with your spouse

If you’re part of a twosome, retirement doesn’t just affect you; it’s a profound lifestyle change for your entire family. Before you take the leap, get on the same page as your spouse.

Will you both be retiring, or will your spouse work longer? If your spouse is planning to maintain a career, will you end up being responsible for more household tasks — and are you OK with that? These questions need to be answered.

You’ll also have to think through how your decision will affect your family finances — especially when it comes to Social Security benefits. If you’re claiming Social Security benefits early, you’ll reduce the monthly benefits you receive for the rest of your life — as well as any survivors benefits your spouse could receive if he or she were to outlive you.

Devise a Social Security claiming strategy with your spouse before you file for benefits that maximizes your combined income, as you can’t easily change your plans once benefits have begun.

2. Figure out where your income will come from

When you no longer have a paycheck coming in, you’ll need funds from other sources.

For most people, retirement income comes from Social Security and savings. A lucky few — mostly government workers — have a defined benefit pension plan to provide guaranteed income. For the rest of us, having enough money invested to supplement Social Security is essential.

To make sure you won’t come up short, add up all your potential sources of retirement funds — from pensions, Social Security, and withdrawals from retirement accounts such as 401(k)s and IRAs — and figure out what your total monthly income will be.

Estimate your Social Security income by visiting mySocial Security to find your benefit amount at full retirement age. Once you’re logged in, there’s a free retirement estimator to help you determine what your benefits will be based on the age you retire. If you’re not ready to create an account, the SSA also has a quick calculator available to estimate benefits by inputting your current year’s earnings, your birth date, and your future retirement date.

To determine the income you’ll receive from investments, you could use the 4% rule, which allows you to withdraw 4% of your account balance in your first year of retirement and then adjust that withdrawal amount each year based on inflation. However, there’s a chance you’ll run out of money by following the 4% rule, so you may want to take another tactic, such as following the advice of experts from the Center for Retirement Research to determine what percentage of your account balance to withdraw annually.

When you add up Social Security income, income from investments, and any other money you’ll have coming, you can make an informed choice about whether it’s feasible to live on the funds available.

3. Set a retirement budget and see if there’s a shortfall

So how do you know if the total income you’ll have will be sufficient to support you?

The best way to tell is to actually make a budget. Factor in all of your fixed costs, such as housing, taxes, and insurance. Add up other expenditures such as traveling, clothing, personal care items, transportation, food, and entertainment. And don’t forget to include saving: Just because you’re no longer investing for retirement doesn’t mean you don’t need to put aside money for other purposes, such as home repairs or emergencies.

Your budget will reveal how much money you’d actually need. If it shows you’ll have plenty of income to cover everything, you’re good to go and can hand in your notice.

If it doesn’t, decide between scaling down your expectations for retirement or increasing your retirement income by working longer, saving more, and earning delayed-retirement credits to boost Social Security benefits.

4. Make a plan for healthcare

One of the big line items in your budget will be healthcare costs.

Seniors often suffer from serious medical conditions, and Medicare doesn’t provide the comprehensive coverage most people believe it does. You’ll have to pick up a lot of prescription costs on your own; you’ll pay premiums and coinsurance expenses; and you’ll need to pay out of pocket entirely for care that isn’t covered, such as nursing home services.

Recent estimates suggest a senior couple in the top percentile for prescription drug use would need $370,000 to be reasonably certain of covering their healthcare needs in retirement. If you don’t have that much, explore options such as working longer and investing in a health savings account or purchasing the most comprehensive Medicare Advantage and long-term care insurance available.

5. Consider how you’ll spend your time

Finally, you need to think about what you’ll actually do during retirement. Some seniors suffer health issues, including depression, when they lose their sense of community and purpose. Have a plan to reduce the risk of becoming lonely and disconnected from the world after retirement.

Depending upon your interests, this plan could include volunteering with local organizations, joining a senior center, babysitting your grandkids, joining a travel group, or taking exercise classes (seniors can often join a gym for free through Medicare’s SilverSneakers program). You could also do some part-time consulting work, either for pay or through volunteer organizations such as SCORE.

Related links:

• Motley Fool Issues Rare Triple-Buy Alert

• This Stock Could Be Like Buying Amazon in 1997

• 7 of 8 People Are Clueless About This Trillion-Dollar Market

Are you ready to retire?

If you’ve gone through these five steps and still feel ready to retire, congrats! You should hopefully have the savings you need to enjoy your golden years.

If you’ve found you’re not quite ready yet, take heart — you’ve taken the important step of identifying the tasks to accomplish and can start checking things off your to-do list.

CNNMoney (New York) First published August 20, 2018: 10:19 AM ET

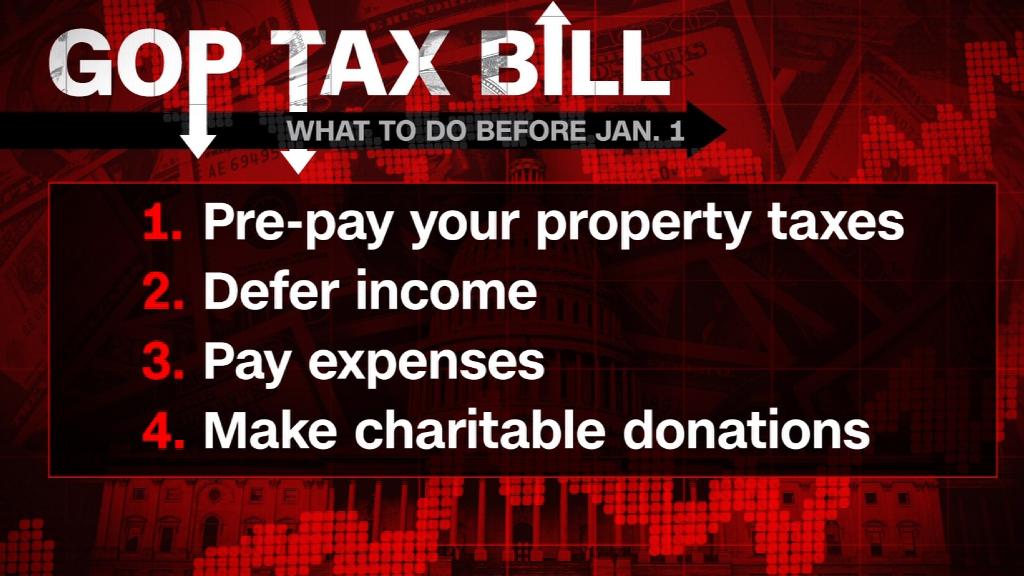

A lot of households under the GOP tax plan, which President Trump is set to sign into law this week, will see a lower tax bill in the next several years.

The nonpartisan Joint Committee on Taxation estimates that in 2019, more than half of filers making $40,000 and up will see an average tax cut greater than $500. That trend holds for income groups over $50,000in the subsequent years measured through 2025.

The Tax Institute at H&R Block provided some scenarios of people with young children, for instance, who could see their tax burden drop by roughly $2,000or more next year.

But here’s the thing: After 2025, all individual tax cuts are set to expire. At the same time, corporate rate cuts are made permanent under the bill.

As a result, by 2027 a large majority of people making less than $200,000 will either see little change in their tax bill or a tax increase relative to what they pay today, the JCT estimates.

Related: Try the CNN tax calculator to see how you may fare under GOP bill

Republicans made individual tax cuts temporary so they could meet budget rules that let them pass their tax overhaul with no Democratic votes.

But don’t worry, they say. A future Congress won’t let middle class tax cuts expire. Recent precedents — like the oft-extended Bush tax cuts — suggest they may be right. Still, there’s zero guarantee of that. After all, a lot can change over eight years.

In any case, there’s another reason you could end up with a tax increase after 2025.

While the cuts are temporary, the GOP tax bill makes permanent another key provision that tax expert Lily Batchelder has described as a “stealth tax increase” for individuals, the effects of which will grow over time.

The money it will raise is a big reason why the cost of the permanent corporate tax cuts will be paid for in the second decade, according to Batchelder, a tax law professor at New York University.

Related: What’s in the final GOP tax plan

The GOP plan introduces a new, slower inflation measure called chained CPI that will apply to inflation-adjusted parts of the tax code. So, for example, the income ranges that apply to each of the seven income tax rates will grow more slowly. So will the value of many tax credits and the income phaseout thresholds for various tax breaks. Those thresholds dictate whether you make too much money to qualify for certain breaks.

The upshot for tax filers is this: Many tax breaks, Batchelder said,“will be worth less over time than they are under current law. And people will gradually be pushed into higher tax brackets over time.”

CNNMoney (New York) First published December 20, 2017: 4:54 PM ET

Kurt Fowler and his wife, Trina, were celebrating their 18th wedding anniversary at a country music festival when the shooting started. Fowler, 41, knew he’d been hit in the ankle and couldn’t run. He hid under the stage until the gunfire ended.

“I knew my foot was completely useless,” said Fowler, a firefighter from Lake Havasu City, Arizona, and a father of three. He underwent surgery, spent nearly two weeks in the hospital and still may need another operation. He also will need rehabilitation and follow-up visits with a specialist.

Fowler has a Blue Cross Blue Shield PPO through his job, but he said he doesn’t know how much he will have to pay out of his own pocket for the care he is receiving. In an era of higher deductibles and limited choice of in-network doctors, however, he knows he could face significant medical bills.

His insurance card says his individual deductible is $5,000 and his coinsurance 20%. He said he didn’t know how much his health plan would cover for out-of-state care.

“It’s a mountain that just doesn’t seem climbable,” said shooting victim Kurt Fowler of his medical bills.

“Medical expenses are astronomical these days,” Fowler said from his bed at Sunrise Hospital & Medical Center in Las Vegas. “It’s a mountain that just doesn’t seem like it’s gonna be climbable, but we are gonna do our best.”

As hundreds of survivors struggle to recover emotionally and physically from the Oct. 1 attack, they are beginning to come to terms with the financial toll of the violence perpetrated against them. Even those who are insured could face untold costs in a city they were only visiting.

The total costs of medical care alone could reach into the tens of millions of dollars, said Garen Wintemute, who researches gun violence at the University of California-Davis.

And that is just the beginning. Many survivors will be out of work for months, if they are able to return at all.

“We really don’t have a good handle on the intangible costs of something like this … the ripple effects on family and friends and neighborhoods when a large number of people have been shot,” Wintemute said.

More than 100,000 people are shot every year in the U.S., according to the Centers for Disease Control and Prevention. That generates about $2.8 billion per year in emergency room and inpatient charges alone, according to a recent study in Health Affairs. The average emergency room bill for an individual gunshot victim is $5,254 and the average inpatient charge is $95,887, according to the study.

Related: Patients pay the price when hospital giants hire your private practitioner

The U.S. senators representing Nevada, Dean Heller and Catherine Cortez Masto, wrote a letter to America’s Health Insurance Plans, an industry trade group, and Scott Serota, CEO of the Blue Cross Blue Shield Association, requesting help with out-of-network bills, copayments and deductibles for the Las Vegas shooting victims. Many of the people who were shot had traveled from other states, including California, Iowa and Tennessee.

California and some states protect consumers from such bills, but Nevada is not one of them, said Sabrina Corlette, a research professor at Georgetown University’s Center on Health Insurance Reforms. But Corlette said most insurers allow patients to request exceptions based on the circumstances.

“In this situation, I imagine most insurers are going to want to be compassionate and work something out,” she said.

The victims and their families aren’t the only ones who will be affected financially by the mass shooting. Taxpayers, too, pick up much of the tab for the health care costs associated with gun violence because many patients are covered by Medicaid and Medicare, two government insurance programs.

Related: Zappos offers to help cover funeral costs of every Las Vegas shooting victim

And hospitals will also be on the hook for some of the care for patients who don’t have insurance. Hospitals in Las Vegas quickly mobilized to treat the hundreds of victims who were streaming in that night, and they don’t know yet how much of the care will be reimbursed.

At Sunrise Hospital & Medical Center, staff treated more than 200 patients. Sunrise plans to file insurance claims and will “be extremely sensitive to the financial status” of patients when considering their out-of-pocket portions, a spokeswoman said.

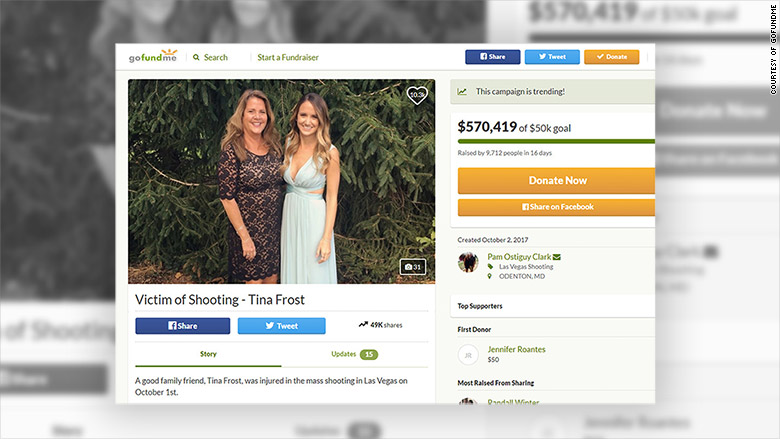

GoFundMe accounts, like this one for Tina Frost, have been helping victims and their families get by.

Valley Hospital Medical Center is encouraging patients to complete paperwork for a state program called Nevada Victims of Violent Crime, which would pay their balances. And Dignity Health’s St. Rose Dominican said it will bill insurers and accept donations but will not require payment from victims.

California victims can also get help with medical expenses and income loss from the California Victim Compensation Board.

In addition, a GoFundMe account started by a Clark County commissioner has raised $11 million thus far. And many survivors have individual GoFundMe accounts.

Related: Doctors in Puerto Rico: ‘Reality here is post-apocalyptic’

Fowler’s GoFundMe page has raised about $39,000. Fowler said he doesn’t have disability insurance so he will rely on the funds to help cover his expenses while he is recovering and missing work.

Michael Caster, 41, who lives in Indio, California, has a GoFundMe account that has raised about $26,000 so far. He’s paralyzed from the waist down after a bullet lodged in his spine.

At Sunrise Hospital, doctors drained the blood from Caster’s lungs and removed some of the bullet fragments. Sitting in a hospital bed 11 days after the shooting, Caster said he didn’t know how much of his care would be covered by his health insurance.

He works in human resources at a California hospital and has a job-sponsored policy with Anthem Blue Cross. “I’ve never really dealt with injury,” he said. “I don’t want to be stuck with a bunch of bills.”

His bills could rise further: That day, he was scheduled to be flown to a rehabilitation center in Colorado for people with spinal cord injuries.

Mary Moreland, whose daughter Tina Frost was shot during the country music festival, said that at first she didn’t understand why so many families were setting up fundraisers. Then, the severe financial strain the shooting would take started to dawn on her.

Now, Moreland said she’s grateful for the nearly $580,000 raised through GoFundMe.

Frost, a resident of San Diego, had emergency brain surgery the night of the shooting. A bullet had pierced her eye and exploded in her brain. As she lay in ICU earlier this month, her mother said small improvements were major milestones. “Today she squeezed my hands,” Moreland said.

Related: Actually Trump is raising health insurance premiums

The next night, Frost came out of a medically induced coma and was later flown to Johns Hopkins Hospital in Baltimore, near her mother’s home. Over the next weeks and months, she will need multiple operations and a slew of specialists, including neurosurgeons, plastic surgeons, occupational therapists and mental health counselors.

Moreland said she cannot even begin to imagine what her daughter’s care will cost. Frost has Blue Cross insurance through her job at Ernst & Young in San Diego, but Moreland said she doesn’t know what the deductible and copayments are.

“Being realistic, knowing what I know about costs of health care, it’s scary,” Moreland said. “But she’s alive. She’s not one of the 58 other people.”

Kaiser Health News, a nonprofit health newsroom whose stories appear in news outlets nationwide, is an editorially independent part of the Kaiser Family Foundation.

CNNMoney (New York) First published October 25, 2017: 6:01 AM ET

There’s going to be a new way for workers to advance their careers in California.

Lawmakers included$100 million in this year’s state budget to create an online community college that will offer certificate and credentialing programs. It will get another $20 million annually.

The plan was proposed by Governor Jerry Brown and backed by California Community Colleges Chancellor Eloy Ortiz Oakley.

The mission is to retrain workers with skills needed in high-demand jobs. There are 2.5 million Californians between the ages of 25 and 34 who are in the workforce but never completed a college degree.

“We’re targeting what we call ‘stranded workers.’ They are in jobs that will eventually be eliminated because of automation and/or they have no real opportunity for economic mobility because all new jobs require some kind of post-secondary credential,” Oakley told CNN.

Roughly one-third of new jobs in the state are expected to require some career technical education that goes beyond high school but not as far as afour-year degree, according to the Public Policy Institute of California.

Related: A degree from this college all but guarantees you a job

The statewide online community college will be tailored to working adults and prepare workers for jobs in growing industries, like advanced manufacturing, healthcare, the service sector, in-home support services, and child development.

The programs are intended to be different than what’s already offered by the state’s community college system. They will usually be shorter than a two-year associate’s degree program. Some will take just three or four weeks, Oakley said.

But many faculty members oppose the creation of a new online school. They say the money would be better spent expanding existing online options.

“Rather than beginning a whole new college and wasting millions of dollars developing a new bureaucracy, the proposed allocation of $120 million would be much better spent expanding the existing community college Online Education Initiative,” a group of independent faculty unions wrote in a letter opposing the measure.

Related: Walmart wants to pay for its workers to go to college

Credentials in information technology support and medical coding will be the first offered at the new online school.

“We’re predicting 10,000 job openings in medical coding over the next four or five years. We will continue to offer it until we see that employer demand was waned,” Oakley said.

A credential in medical coding is not currently offered by California’s community college system, which is one of the biggest in the country and has 114 campuses.

The costwill be comparable to the $46 per credit charged by the traditional community colleges. But students may be charged on a per-module or subscription system, Oakley said.

The plan is to begin enrolling students in the new online college by the end of 2019.

The state budget was approved by lawmakers on Thursday. The governor has until June 30 to sign the legislation.

CNNMoney (New York) First published June 19, 2018: 11:37 AM ET

An investing earthquake is underway and it’s threatening to end traditional money management as we know it.

Investors are pouring their money into so-called passive index funds that blindly track market indexes using computers.

It’s a shift that is coming at the expense of funds that are run by mere mortals, aka invesment managers, who try to pick stocks that will outperform the market.

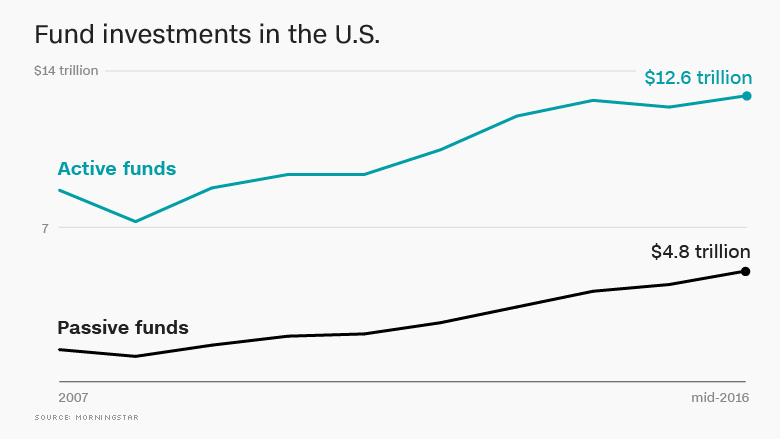

The trend is especially pronounced in the United States, where 28% of the industry’s $17 trillion in assets are currently invested in passive funds, up from just 13% in 2008, according to data from market research firm Morningstar.

American investors have plowed a total of $671 billion into passive funds since the start of 2015, while pulling $257 billion out of so-called active funds run by managers over the same period.

Prominent BlackRock(BLK) CEO Larry Fink predicted this week that regulatory changes in the industry will encourage even more money to flow into these funds.

“We are likely to see a historical shift on how assets are being managed,” he said. “[Investors] will use [passive funds] more and more at the center of their portfolios.”

BlackRock’s(BLK) popular iShares business, which offers investors passive exchange-traded funds (aka ETFs), saw $51 billion in net inflows over the past quarter while the firm’s active funds brought in less than one-tenth that amount.

U.S. investors have historically put more money into active funds. But the passive fund industry is growing at a much faster rate. It now has $4.8 trillion in assets under management.

While it’s tempting to invest with top investment managers who promise to outperform the market, research has shown that this strategy often results in smaller returns.

“Actively managed funds have generally underperformed their passive counterparts, especially over longer time horizons,” said Morningstar researchers in a recent paper.

The reason for the lackluster performance of active funds typically comes back to investment fees — which are much higher at active funds. (Computer algorithms don’t have kids to feed back at home!)

Related: How should I invest a $250,000 windfall?

But some market strategists warn that passive investing is becoming a crowded trade, with too many people hopping onto the bandwagon.

“Indexing and ETFs offer tremendous value as part of the market, but they should not become the market. If this is an investor’s singular approach to the markets, it represents a pursuit of mediocrity,” said Mike O’Rourke, chief market strategist at JonesTrading.

CNNMoney (London) First published October 20, 2016: 6:36 AM ET

Joining a growing number of luxury auto makers, Audi unveiled a new all-electric SUV. Called the E-Tron, the SUV will be available in Europe later this year and in the United States next spring.

Audi said it is taking refundable $1,000 deposits for the E-Tron starting now. Prices will start at about $75,000 or $86,700 for well-equipped “First Edition” models.

It’s the first of three new electric vehicles Audi will introduce over the next few years. The German luxury automaker, which is part of the Volkswagen Group(VLKPF),also announced it ispartnering with Amazon to handle installation of home charging stations for E-Tron buyers.

The E-Tron was revealed at an event on the San Francisco waterfront. Hundreds of drones formed Audi’s four ring logo over a former Ford factory turned event space.

The SUV was unveiled here because the E-Tron was designed with the US market especially on mind, Audi executives said.

While it might not generate the excitement of a Tesla unveiling —that company receivedhundreds of thousands of dollars in deposits for its Model 3 within hours of that car’sdebut— the E-Tron increases the competitive pressure.

The E-Tron follows Jaguar’s I-Pace electric SUV. Mercedes and BMW also recently unveiled electric SUVs that will go on sale within the next couple of years.

These offerings are all SUVs mostly because the market, in general, has shifted heavily in that direction.

“We wanted to be in the SUV space because we saw the growth and we wanted to be in the sweet spot of the market,” said Filip Brabec, Audi’s vice president for product development.

Car shoppers considering an electric car today are no longer interested in their vehicle looking radically different from anything else on the road, said Brabec.

The Audi E-Tron has a trademark looking Audi grill that lets in air to help cool the battery.

The E-Tron looks, quite clearly, like an Audi SUV. It even has Audi’s famous trapezoidal grill, a key branding feature, despite not needing a radiator. The grill allows air to pass through under the battery to provide some additional cooling.

There are some unique attributes, though. The E-Tron stands a little wider than Audi’s other SUVs. Slats running across the rear bumper draw attention to the car’s lack of tailpipes, while there are lights in the front that are designed to look like the bars of a charge status indicator.

The Audi E-Tron has two touch screens inside and, in European models, cameras instead of side mirrors.

In Europe, the E-Tron won’t have traditional side mirrors. Instead, it will have a camera on each side where mirrors would ordinarily be. The views from those cameras will be displayed on screens inside the vehicle.

That system will not be available in theUnited States because safety regulations here don’t allow for it. Audi executives said they are working with the National Highway Traffic Safety Administration to bring this feature to the American market.

A dark colored section along the side of the E-Tron calls out the fact that there is a battery pack there.

With two electric motors, the all-wheel-drive SUV can accelerate from zeroto 60 miles an hour in 5.5 seconds and it has a top speed of 124 miles an hour. It will be able to tow as much as 4,000 pounds. Audi has not yet announced what its driving range will be on a full charge.

When the E-Tron is cruising, rather than accelerating, it is driven mostly by the rear motor. Engineers put a heavy emphasis on recuperating as much energy as possible while driving. That’s generally done as a vehicle brakes or slows by allowing the wheels to push the electric motors, which then act as generators.

In the E-Tron, the driver will be able to select how aggressively the car uses this system, allowingfor“one pedal” driving in which taking pressure off the accelerator pedal will slowthecar to a full stop using only the motors.

As with other Audi vehicles, the driver will also be able to select different driving modes, from comfortable to sporty, that will alter suspension stiffness, steering responsiveness and how aggressively the SUV accelerates. The SUVs ground clearance is also adjustable by as much as three inches.

Buyers will be able to purchase a home charging system and have it installed by Amazon Home Services. The installation can be ordered online. Pricing will vary depending on each homeowner’s needs.

Audi plans to release two more electric vehicles in the next two years and a total of 12 by 2025.

CNNMoney (San Francisco) First published September 18, 2018: 12:08 AM ET

How can I protect my investments against inflation?

Even as your investments increase in value, inflation can eat away at what they’re worth.

There are things investors can do to hedge the immediate effects of inflation, or earn a return that outpaces inflation over time. But it can be hard to predict.

“After-inflation returns are the only ones that matter for investors in the real world,” says Robinson Crawford, an investment adviser with Montebello Avenue.

Even if inflation is currently rising more slowly than analysts predicted, it’s better to be prepared.

Financial advisers say one of the most consistent hedges against inflation is a properly diversified stock portfolio.

Equities have historically outpaced inflation, says Sean C. Gillespie, a financial planner with Redeployment Wealth Strategies says that while there is inherent volatility in a stock portfolio, “equities are a long-term asset for your plan just like inflation is a long-term threat.”

To figure out where to put your money in the stock market, investors could look to a total return strategy that relies on equities to provide positive inflation-adjusted returns over the long term.

“Of course, investors have to accept more risk when investing in stocks and endure periods when the returns have not outpaced inflation,” says Dejan Ilijevski, an investment adviser at Sabela Capital Markets. “Although some investors may assume that higher inflation leads to lower stock performance, US market history shows that nominal annual stock returns are unrelated to inflation.”

Gold and commodities

Gold and commodities have been standard havens from inflation for investors.

“Traditionally commodities and gold have been good inflation hedges,” says Stephanie Bucko, a chartered financial analyst and co-founder of Mana Financial Life Design. But she says it is important to take into account the US dollar’s strength as part of this equation.

“We like oil exposure, as this impacts our clients on a day-to-day basis related to gas prices, but it also provides a good inflation hedge,” says Bucko, adding that we saw this in the 1970s as inflation doubled and nominal oil prices skyrocketed.

But commodity markets, for the unfamiliar, can be complex and risky.

“Commodities are volatile, more so than stocks, which means that adding commodities to a portfolio may increase real return volatility, offsetting the benefits of hedging,” says Ilijevski.

Real estate is the ultimate hard asset in times of inflation since it will see price appreciation. Financial advisers suggest investors find a place for real estate in a portfolio.

Investors can gain exposure to real estate by directly owning commercial or residential property, or by investing in real estate investment trusts (REITs).

Real estate is a sound investment, says Crawford. “But I would caution that if you’re not increasing rent in your real estate, you aren’t fighting inflation.”

Short term bonds and TIPS

Short-term bonds and Treasury Inflation-Protected Securities (TIPS) are investments that are a hedge against inflation.

“Hedging seeks out asset classes that tend to positively correlate with inflation,” says Ilijevski.

For example, he says, short-term maturities allow bond-holders to more frequently roll over the principal at higher interest rates. This helps inflation-sensitive investors keep up with short-term inflation.

Similarly, TIPS, issued by the government, are also a fixed-income security hedge against inflation. Their principle is adjusted to reflect changes in the Consumer Price Index. When CPI rises, the principle increases, resulting in higher interest payments.

“TIPS absolutely merit a place in a US investor’s portfolio, especially those with significant bond holdings,” says Crawford. “The main issue is that they increase in value in conjunction with the CPI, which many would argue is not an accurate inflation measure.”