Unemployment keeps falling and home prices keep going up. It’s a great recipe for a strong housing market.

Nothing has been able to stop the housing boom — not even higher interest rates.

Luxury home builder Toll Brothers(TOL) said Tuesday that demand for its houses was strong across the country — the company signed a record number of contracts last quarter.

Toll Brothers reported quarterly financial results that easily topped forecasts and raised its outlook for the year, citing a backlog of new homes for the third quarter.

Higher rates do not seem to be an issue for prospective buyers, mainly because the job market remains strong and housing prices are rising.

The company said that the average price of its homes in the most recent quarter was $851,900, compared to $791,400 a year ago. And Toll Brothers expects that prices for the current quarter will range between $840,000 and $870,000.

The only weak spot was California, where demand cooled a bit.

Toll Brothers executive chairman Robert Toll said the company believes the new home market can continue to grow in the coming years — especially as people seek to cash in on the rising value of their current home and trade up.

As the value of people’s homes increases, empty nesters and homeowners looking for bigger houses have more equity to work with, Toll said in the company’s press release. He also expects those two groups and Millennials will fuel demand for new homes in the coming years.

Shares of Toll Brothers surged more than 11% on the solid earnings Tuesday — but the stock is still down 20% for the year.

The results are the latest sign that the recent homebuilder stock slump may have been an overreaction. Investors feared that rate hikes would weaken demand for homes. That hasn’t happened yet.

Rival builder Lennar(LEN) also reported healthy quarterly results in late June.

Retail giant Home Depot(HD) just posted strong numbers last week as well, another sign that people continue to spend on their houses. Home Depot rival Lowe’s(LOW) will report results Wednesday and analysts are expecting a nearly 30% jump in earnings.

CNNMoney (New York) First published August 21, 2018: 10:45 AM ET

Buying a home is a major commitment and many factors determine what a mortgage lender is willing to offer you. Tell us a little about your finances and the type of property you’re looking to buy to get a sense of what you can afford.

Before you start shopping for a new home, you need to determine how much house you can afford.

One way to start is to get pre-approved by a lender, who will look at factors such as your income, debt and credit, as well as how much you have saved for a down payment, to come up with loan amount you can afford.

One rule of thumb is to aim for a home that costs about two-and-a-half times your gross annual salary. If you have significant credit card debt or other financial obligations like alimony or even an expensive hobby, then you may need to set your sights lower.

Another general rule of thumb: All your monthly home payments should not exceed 36% of your gross monthly income.

This calculator can give you a general idea of what size mortgage you can afford.

The antique look of the Mercedes-Benz G-class SUV is a big part of its rugged charm. So much so, in fact, that even though the 2019 version is completely new, Mercedes designers have made sure it still looks old.

Most passenger cars are completely redesigned roughly every five years to keep up with changing tastes. But is the first time the G-class has been fully redesigned in 40 years. There have been improvements over the decades — but never a thorough wheels-to-roof makeover like this.

To make the point, Mercedes placed a current-generation G-class encased in a massive cube of amber-colored resin outside the auto show. Not coincidentally, it looks like a dinosaur-era bug trapped in amber, a la Jurassic Park.

G-class fans like the SUV’s classic truck-like appearance. It is definitely not a crossover SUV, even though many of its owners in the United States may use it the same way someone might use a Honda CR-V.

Mercedes-Benz encased an older G-class in amber-colored resin.

But the G-class not only looks and drives very differently from a CR-V, it also costs a good bit more. Prices for the current version start at about $124,000 in the U.S., its biggest market.

The G stands for Geländewagen which means, literally, “terrain car” or, less literally, SUV.

The new Mercedes-Benz G-class retains the classic look of the original.

The all-new version was unveiled at an event inside a decayed abandoned theater in Detroit. The introduction featured towering jets of flames, a G-class climbing an impossibly steep looking hill, and an appearance by Arnold Schwarzenegger. (The connection is that Schwarzenegger was born near Graz, Austria, where the G-class is built. Also, he’s strong.)

Mercedes designers made every effort to maintain the Lego-built appearance of the G-class, including exposed door hinges, and even the resonating metallic thunk sound of its doors closing. Engineers also went to the trouble of designing the turn signal lamps that stand up on the front of the car so they retract on impact. That retains the classic look while still complying with modern pedestrian protection regulations, which require anything that sticks out on the front of a vehicle that could stab or poke a person must collapse out of the way in a crash.

They did make some changes to modernize the vehicle and add a little more comfort. For instance, it’s slightly larger all around. Despite its size, though, rear seat legroom remains a little snug by SUV standards. But there’s still enough headroom to comfortably go off-roading in a top hat. The modern LED headlights, while still round, are noticeably more complex.

Modernization is most noticeable inside the new G-class.

The differences on the inside are much more noticeable. For instance, it hasa large central screen, like other Mercedes cars, and the gauge cluster behind the steering wheel has also been replaced by a computer screen. It displays classic-looking round gauges, however, so the new tech doesn’t ruin the old looks.

CNNMoney (New York) First published January 16, 2018: 3:27 PM ET

You’ve been dreaming of owning a home for years, and now you’re finally ready to make the leap. You’ve found the perfect place and may have even started deciding where to put the furniture, but you still have one big obstacle standing in your way: getting a mortgage.

If you’ve never bought a home before, the whole process can seem a little confusing. One of the first things you have to figure out is whether you should get a fixed-rate or adjustable-rate mortgage. Most people choose the fixed-rate mortgage without even thinking about it, but there are situations where an adjustable-rate mortgage may be a better fit.

How fixed-rate mortgages work

Every mortgage charges interest in order to make the deal worth it for lenders. With fixed-rate mortgages, you lock in a single interest rate for the lifetime of your loan. Usually, the payment period is 30 years, but it can be 20 or 15 if you want to pay off your home more quickly.

The reason fixed-rate mortgages are so popular is that they’re more predictable. You know exactly how much money to set aside out of your paycheck each month to cover the bill. Plus, if interest rates rise, you don’t have to worry about your monthly mortgage payment rising accordingly.

The disadvantage is that if mortgage rates go down and you’d like to capitalize on this, you’ll have to refinance — and that means spending a few thousand dollars in closing costs. Fixed-rate mortgages also have higher starting interest rates than adjustable-rate mortgages, and that may limit how much home you’re able to buy.

How adjustable-rate mortgages work

As the name implies, adjustable-rate mortgages (ARMs) have interest rates that change over the lifetime of the loan. Most ARMs these days are hybrids, which means they have an initial fixed-rated period, after which the interest rate begins to change, usually once per year. You may see this written as 5/1 or 7/1. This means that you get five or seven years of a fixed interest rate, and after that, the interest rate — and your payments — will be adjusted every year.

The risks of ARMs are clear. When your interest rate can change, it’s possible that your payments could become so expensive that you can’t keep up with them. If your monthly payments during the initial fixed-rate period would put a strain on your budget, an ARM isn’t a good choice for you. Before taking out an ARM, be sure to get a Truth in Lending disclosure from your lender, which should list the maximum amount your monthly mortgage payment could reach. Make sure you’re comfortable with this amount before you sign on the dotted line.

But there can be times when an ARM is the smarter choice. Starting interest rates on ARMs are usually lower than on fixed-rate mortgages, so your monthly payments will likely be lower for at least a few years. And if you find yourself in an environment where mortgage interest rates are declining or holding steady, your interest rates may not increase significantly even after the fixed-rate period is up.

If interest rates begin to decline, your monthly payments may actually decrease, though not all ARMs allow this, and they often put a cap on how low your payments can go. Typically there are also caps on how much your payments can increase, both annually and over the lifetime of the loan. You may see this written as 2/2/5 or something similar. The first number reflects the greatest amount by which the interest rate can rise in the first year after your fixed-rate period ends — in this case, 2%. The second number represents the most it can change every year thereafter, and the third number represents the most it can change over the lifetime of your loan.

Related: More on buying a home

To put this in perspective, let’s say you buy a $250,000 home with a 30-year 5/1 ARM, a 4% initial interest rate, and 20% down. Your initial monthly payment would be $955. In an ideal world, that number wouldn’t increase over the lifetime of the loan, and you’d get the whole house for about $344,000, factoring in interest.

However, that’s nearly the best-case scenario. Now let’s consider the worst-case scenario. Imagine that, after the initial fixed-rate period, your interest rate rose by 0.25% each year until it reached the maximum increase of 5%, bringing your interest rate to 9%. You’d end up paying $419,000 over the lifetime of the loan, and your monthly payment would climb to $1,323.

These are extreme scenarios, and in reality, the price you ultimately paid for your home would likely fall somewhere in the middle. However, you should keep in mind that if your ARM’s interest rate reaches its cap, it could cost you tens of thousands of dollars in additional interest payments.

Which type of mortgage is right for me?

Fixed-rate mortgages are usually the better choice for most people. This is especially true if you plan on being in your home for more than five years or if interest rates are historically low, as they are now.

Related links:

• Motley Fool Issues Rare Triple-Buy Alert

• This Stock Could Be Like Buying Amazon in 1997

• 7 of 8 People Are Clueless About This Trillion-Dollar Market

You may want to consider an ARM if you’ll only be in the home for a few years, if you think interest rates will decrease, and/or you expect your income to rise enough to absorb higher mortgage payments. Before you sign up for an ARM, though, it’s important to calculate how much your mortgage payment could change over the lifetime of your loan to make sure it’s still something you could afford.

CNNMoney (New York) First published August 8, 2018: 10:19 AM ET

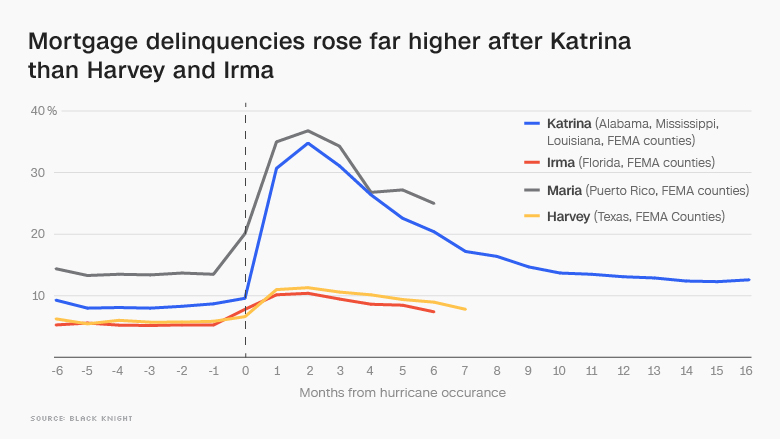

After Hurricane Harvey soaked Houston with 51 inches of rain last August, Amir Befroui, a foreclosure defense specialist at Lone Star Legal Aid, started planning for a very busy spring.

That’s when the 90- and 180-day break on payments that mortgage companies typically give homeowners who have been hit by unexpected events like natural disasters would start to run out.

But so far, few hurricane-related foreclosure cases have been coming across his desk.

“We are starting to see a trickle,” Befroui says. “I suspect it’s going to be a gradual increase. I don’t think it’s going to be a tidal wave like the one that happened after Ike.”

According to real estate analytics firmAttom Data Solutions, foreclosure starts in hurricane-affected areas of Texas and Floridarose in the first quarter of 2018, but still remained below pre-hurricane levels.

In Houston, for example, foreclosure starts had been slightly elevated due to the oil price crash of 2015 and 2016. Not counting a dip at the end of 2017, the first quarter was as low as it’s been in more than 12 years, with 1,184 foreclosure starts. That’s a big difference from Hurricane Ike in late 2008, where the storm exacerbated a mounting economic crisis that spurred 7,280 foreclosure starts in just one quarter.

Related: Devastating hurricanes dealt corporate America a major blow

Even more encouraging, the number of people seriously delinquent on their loans in hurricane–affected areas of Texas and Florida continued to sink after spiking over the winter. Thousands of people were able to bring their mortgages current again after taking advantage of post-storm forbearances from their lenders.

Given how damaging foreclosures can be for property values, credit scores and community stability, it appears the Gulf Coast has managed to dodge apotential hurricane housingdisaster. At least, so far.

Part of that is due to coordinated efforts by industry groups and consumer advocates who helped create better options for homeowners to modify their loans afterthe break on mortgage payments ends. But more importantly, reforms to mortgage policies following the financial crisis had already fostered a healthier housing market to begin with.

Homeowners went into last year’s disasters in a better place financially than they were during Hurricanes Ike, which hit in 2008, Sandy in 2012, and even Katrina in 2005.The irresponsible lending practices of the late 1990s and 2000s had largely been ended by the Dodd-Frank Act and the Consumer Financial Protection Bureau, which raised standards for mortgage underwriting and implemented protections for borrowers facing foreclosure.

“People who’ve gotten mortgages post-CFPB, they don’t have loans for the most part that economically they could never have afforded,” says Ira Rheingold, executive director of the National Association of Consumer Advocates.

Related: Disaster costs jumped over 60% this year to $306 billion

Across the United States, the number of properties in active foreclosure fell in March to the lowest level since late 2006, according to the real estate data firm Black Knight.

But in the case of natural disasters,programs aimed at helping distressed homeownersaren’t alwayshelpfulenough. Mortgage modification programs administered by Fannie Mae, Freddie Mac, Ginnie Mae, the Veterans Administration, and the Federal Housing Administration — which now back about 70% of the U.S. housing market — require lots of documentation that’s hard to pull together if your home is literally underwater.

A Houston home flooded after Hurricane Harvey hit.

Homeowners were snarled in endless paperwork after Hurricane Sandy hit in 2012, with each government housing agency requiring different policies and homeowners owing balloon payments that came due immediately once the forbearance period ended.

So as the 2017 hurricane season got started in earnest, D.C.’s housing finance wonks came to government agencies with one fundamental ask: Design a uniform option that can give homeowners a break on their mortgages without getting them in trouble when the bills come due.

“We were unsuccessful during Sandy,” says Meg Burns, a former Department of Housing and Urban Developmentofficial who now heads housing policy at the Financial Services Roundtable, which represents lenders and servicers. “That’s what informed our thinking to get all of the government entities around the table to make some consistent policy.”

Along with automatic forbearances for homeowners in hurricane-affected areas, Fannie, Freddie and the FHA came up with an option that allows borrowers to make the payments they skipped during the months after the disaster at the very end of the loan — without going through a modification that could force them to take on a higher interest rate.

Related: Hurricane-struck businesses face rebuilding again

“It’s a different world now,” says Sara Singhas, associate regulatory counsel at the Mortgage Bankers Association, referring to the recent departure from rock-bottom interest rates. “Especiallyfor people who are performing on their loans, we wanted to make sure we don’t put them into a worse financial position than they were prior to the disaster.”

These provisions, however, are only temporary and will sunset if they aren’t renewed. “I would feel a lot better if they codified what we did,” says Peter Muriungi, head of mortgage servicing for Chase Bank, which had 450,000 customers affected by the 2017 storms.

On the ground, housing counselors say that lenders have been more willing to work with people who can prove they have been a victim of a hurricane. That kind of patience is not typically afforded to people facing foreclosure for economic reasons, such as spiking property taxes, which have become more of a problem in the Houston area in recent years.

“The large national servicers, once they get it into their head that this is a Harvey case, then it gets moved over to the disaster recovery center rather than the traditional foreclosure side,” says Sherrie Young, executive director of the Credit Coalition in Houston.

Maurine Howard has struggled to keep her mortgage payments from ballooning after her home was damaged during Harvey.

But not everybody takes action in time to receive that kind of assistance, and not everybody qualifies when they do. For those who lost jobs as a consequence of the hurricanes or were already behind on their payments before disaster struck, options start to narrow.

That’s why thousands of people are still facing the prospect of losing their homes, and many more could run into that situation as banks lose patience in the coming months. Aid groups worry about the people who haven’t yet asked for help.

“I think the biggest problem lies with the folks who don’t reach out,” says Glenda Kizzee, a housing counselor at the Houston Area Urban League. “They’re going to utilize whatever resources they have to rebuild the home, and sometimes miss the payment on the home, which is just going to make it worse. By that time, our resources are limited in what we can do.”

The biggest headaches, counselors say, arisewith smaller servicers that have fewer resources to work with homeowners in trouble.

Take Maurine Howard, whose stately home near Addicks and Barker reservoirs in Houston was inundated when the Army Corps of Engineers released the floodgates in order to avoid a breach. She paid off the three months of mortgage payments after her forbearance ended, but the mortgage company still bumped up her monthly payment from about $1,350 to $1,700.

Months of phone calls, she says, still haven’t managed to fix the problem, while she racks up credit card debt to make fixes on the house.

“Through the process of Harvey, dealing with the mortgage company has been a nightmare,” Howard says, amid stacks of paper laid out on a bed in one of the few undamaged rooms of the house. “It’s never ending. You take two steps forward and five steps back.”

CNNMoney (New York) First published April 22, 2018: 10:09 AM ET

Everyone knows weddings are pricy. Meghan Markle’s upcoming wedding to Prince Harry in the UK will take things to the next level.

Seasoned wedding planners estimate the cost for the May 19 wedding could reach £1 million ($1.4 million) or more. The cost for special security raises the bill much further.

Still, even the most lavish weddings don’t generally exceed £10 million ($13.5 million), according to Jamie Simon, head of events at the luxury British event management firm, Banana Split.

“There’s only so many ideas you can come up with before you [start] inventing ways to spend money,” he said.

Plus, the couple is getting some things for free. Swipe through to review a breakdown of the expected costs.

Homebuyers are proving to have some pretty thick skin.

Home prices are still rising, supply is getting leaner, mortgage rates are going up and competition is intense.

Yet despite all the headwinds, buyers seem to be largely resolute.

“Buyer demand is still there and strong,” said Nela Richardson, chief economist at Redfin. “The only thing slowing demand is the lack of things to buy.”

Homes sold 7% faster in March compared to a year ago, according to realtor.com, while prices were 8% higher. At the same time, housing supply was down 8%.

Related: Renting vs. Buying: What can you afford?

And it doesn’t look like the search will be getting easier anytime soon.

“Very strong home prices are due to a real lack of supply … and prices are likely to continue to run well above inflation and income growth all over the country,” said Leonard Kiefer, deputy chief economist at Freddie Mac.

The rate on a 30-year fixed mortgage climbed to 4.47% last week, the highest level since 2014.

“The same $250,000 budget won’t buy what it would have bought you last year,” said Danielle Hale, chief economist for realtor.com. “But people are still finding ways to make that $250,000 work.”

Experts predict rates will climb to around 5% by the end of the year. That could be the thing that finally cools off the market and pushes some buyers onto the sidelines, according to Keith Gumbinger, vice president of HSH.com.

“There is an important psychological point when you cross 5%,” he said.

But buyers aren’t giving up yet.

Related: Looking to buy your first home? Good luck with that

Chris Gaudreau and his fiancé, moved up their plans to buy a home as they watched prices and interest rates move higher.

“We figured we had to pull the trigger before we get priced out of the market,” Gaudreau, 39, said.

They were looking in the Denver area and set a budget of $400,000, but were really hoping to stay around the $380,000 mark. They started their house hunt in February, and the search was intense.

Their mornings started with reviewing new inventory that hit the market overnight. On good days, there would be 20 new listings. But on other mornings there were no new homes available.

“That was frustrating,” he recalled. He estimated that they looked at more than 70 homes over five weeks. Once they saw nine in a single day.

Their list of “must haves” evolved over their search as they came face-to-face with the reality of what was available.

“It was insane and so much pressure. And if you liked something, you couldn’t go home and sleep on it — you had to put an offer in right away,” he said.

Related: Home sellers are making huge profits. So why aren’t more selling?

The lack of homes on the market is constraining sales as sellers are hesitant to list.

Supply at the starter home level is particularly weak in markets across the country.

“Entry-level buyers are going to have the biggest challenge because that is where inventory declines have continued to decline the most, and that is where the market is most competitive,” said Hale.

Selling the home will likely be easy, but finding a place to move into is another story.

Plus, many current homeowners have likely refinanced to lock in rock-bottom rates, and taking out a new mortgage could mean higher borrowing terms.

Home buyers need to act fast when they find a home. Last year, almost a quarter of all homes sold for more than the asking price, according to a recent report from Zillow.

That’s one reason experts recommend knowing exactly how much you can afford and are comfortable spending on a home. It’s also a good idea to get pre-approved for a loan to make your offer stronger andbe ready to move right away.

Gaudreau and his fiancé ended up bidding on eight houses. Their winning offer was for a three-bedroom, two-and-a-half home in Aurora. The home was listed at $360,000 and they offered $370,000. They are set to close this week.

Are you currently looking to buy a house or recently become a homeowner? We want to hear from you. Tell us about your experience and you could be included in a future story

CNNMoney (New York) First published April 25, 2018: 10:13 AM ET

Accurately calculating your monthly mortgage payment can be a critical first step when determining your budget. Enter your details below to figure out what you might pay each month.

Looking to buy a home? It’s important to take out a mortgage that you can reasonably afford.

A mortgage is a home loan that is usually paid back in fixed amounts over a period of time – typically 15 or 30 years. Each payment includes a portion that goes toward the mortgage principle, and another portion that goes toward interest charged by the lender.

Most experts recommend that your monthly mortgage payment should not exceed 35% of your gross income. But that is the upper end. Other models are more conservative and suggest 25%, in order to keep your debt-to-income ratio lower. A middle-ground recommendation says you shouldn’t put more than 28% of your monthly gross income toward your mortgage payment.

And don’t forget to consider additional costs associated with owning a home, such as utilities, taxes, maintenance, which will add to your monthly costs.

This calculator can help you determine what your monthly payments will be, based on how much money you plan to borrow for your home purchase.